1. Introduction to Forecasts

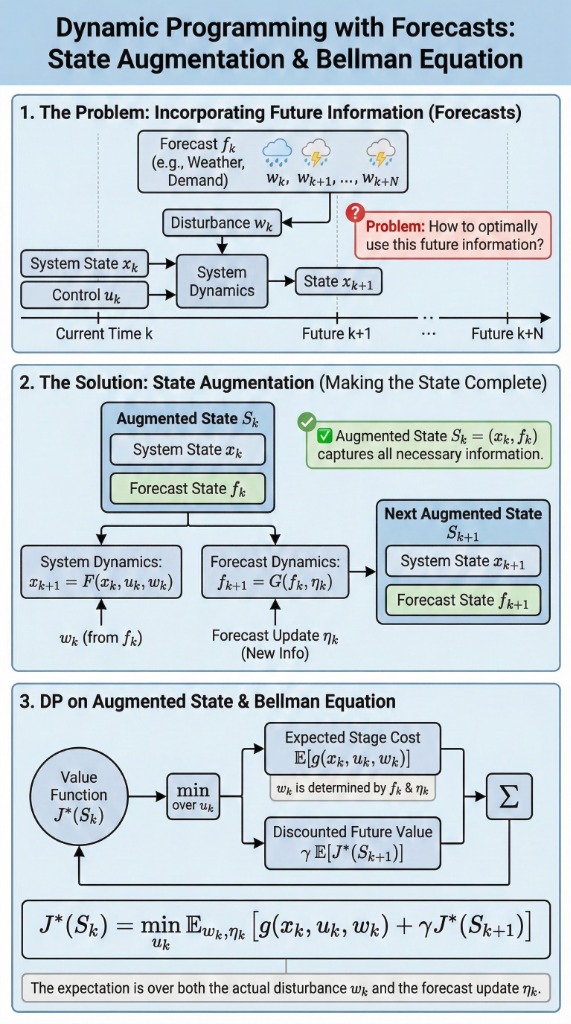

At time \(k\), the controller receives a forecast \(y_k\). This forecast changes our belief about the upcoming disturbance \(w_k\).

Weather

Rain probability affects agriculture decisions.

Interest Rates

Economic forecasts affect investment.

Demand

Inventory needs based on market trends.

Forecast Model

If the forecast is \(y_k = i\), then the disturbance \(w_k\) is selected according to a specific probability distribution \(P_i\).

2. The Forecasting Equation

The forecast itself evolves over time:

\[ y_{k+1} = \xi_k \]Where \(\xi_k\) is a random variable representing the next forecast.

Forecast Evolution

3. Augmented System

We combine the physical system state \(x_k\) and the information state (forecast) \(y_k\) into a new augmented state.

Augmented State Definition

\[ \tilde{x}_k = \begin{bmatrix} x_k \\ y_k \end{bmatrix}, \quad \tilde{w}_k = \begin{bmatrix} w_k \\ \xi_k \end{bmatrix} \]The system dynamics become:

\[ \tilde{x}_{k+1} = \begin{bmatrix} f_k(x_k, u_k, w_k) \\ \xi_k \end{bmatrix} \]Augmented System Diagram

4. DP Algorithm with Forecast

The DP algorithm is applied to the augmented state \((x_k, y_k)\).

Bellman Equation

\[ J^*_k(x_k, y_k) = \min_{u_k} E_{w_k} \left\{ g_k(x_k, u_k, w_k) + \sum_{i=1}^{m} p_i J^*_{k+1}(f_k(x_k, u_k, w_k), i) \mid y_k \right\} \]Note: The expectation \(E_{w_k}\) depends on the current forecast \(y_k\).

5. Summary Infographic

6. Test Your Knowledge

1. A forecast \(y_k\) primarily affects:

2. The "Forecasting Equation" \(y_{k+1} = \xi_k\) implies:

3. In the augmented state \(\tilde{x}_k = (x_k, y_k)\), the variable \(y_k\) is:

4. The DP algorithm expectation is conditional on:

5. Can forecasts be influenced by control actions?

🔍 Spot the Mistake!

Scenario 1:

"The forecast \(y_k\) is always a perfect prediction of \(w_k\)."

Scenario 2:

"We can solve the problem without augmenting the state with \(y_k\)."

Scenario 3:

"The next forecast \(y_{k+1}\) depends on the current disturbance \(w_k\)."