1. The Linear Quadratic Problem

We explore a classical problem with linear dynamics and quadratic cost. This provides deep insights into the Bellman equation.

General Form

System: \( x_{k+1} = Ax_k + Bu_k \)

Cost: \( g(x, u) = x^TQx + u^TRu \)

- \( Q, R \) are positive definite symmetric matrices.

- No control constraints.

One-Dimensional Version

To simplify, we look at the scalar case:

\[ x_{k+1} = ax_k + bu_k \] \[ \text{Cost} = \sum_{k=0}^{\infty} (q x_k^2 + r u_k^2) \]This scalar version captures the core algorithmic challenges.

2. The Riccati Equation

The optimal cost is quadratic: \( J^*(x) = K^* x^2 \).

The scalar \( K^* \) satisfies the Riccati Equation \( K = F(K) \), where:

\[ F(K) = \frac{a^2 r K}{r + b^2 K} + q \]The optimal policy is linear: \( \mu^*(x) = L^* x \).

Fig 1: The Riccati Operator \( F(K) \)

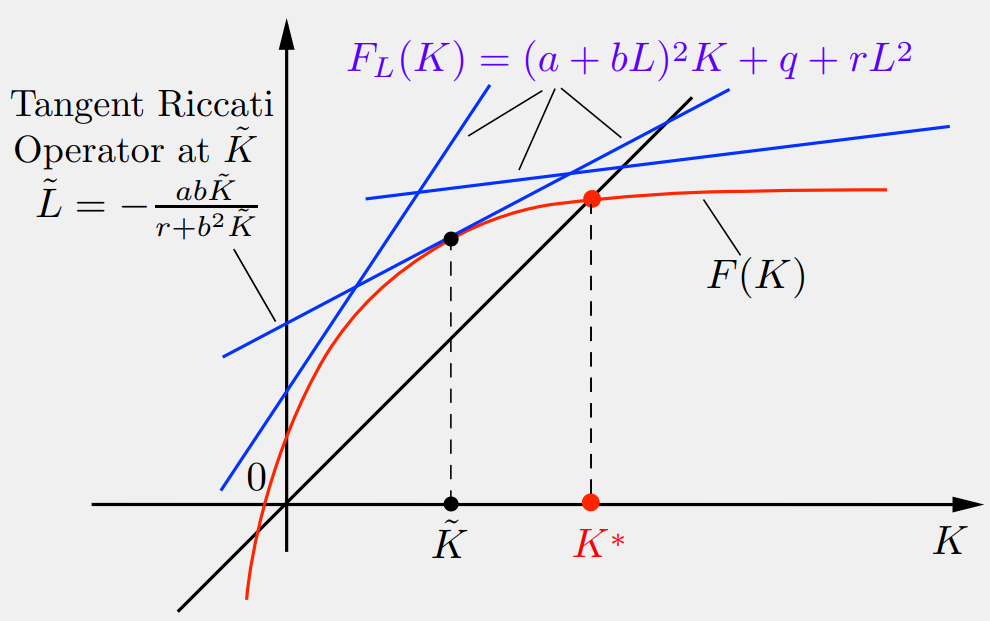

Stable Linear Policy

For a stable linear policy \( \mu(x) = Lx \) (where \( |a+bL| < 1 \)), the cost is \( J_\mu(x)=K_L x^2 \).

\( K_L \) is the unique solution to the linear equation:

\[ K = F_L(K) = (a + bL)^2 K + q + rL^2 \]

Fig 2: Riccati Equation for Stable Policy

3. Value Iteration (VI)

The VI algorithm generates a sequence of quadratic costs \( J_k(x) = K_k x^2 \).

\[ K_{k+1} = F(K_k) \]Starting from any \( K_0 \geq 0 \), it converges to \( K^* \).

VI Convergence Animation

Visualizing convergence of K to K*

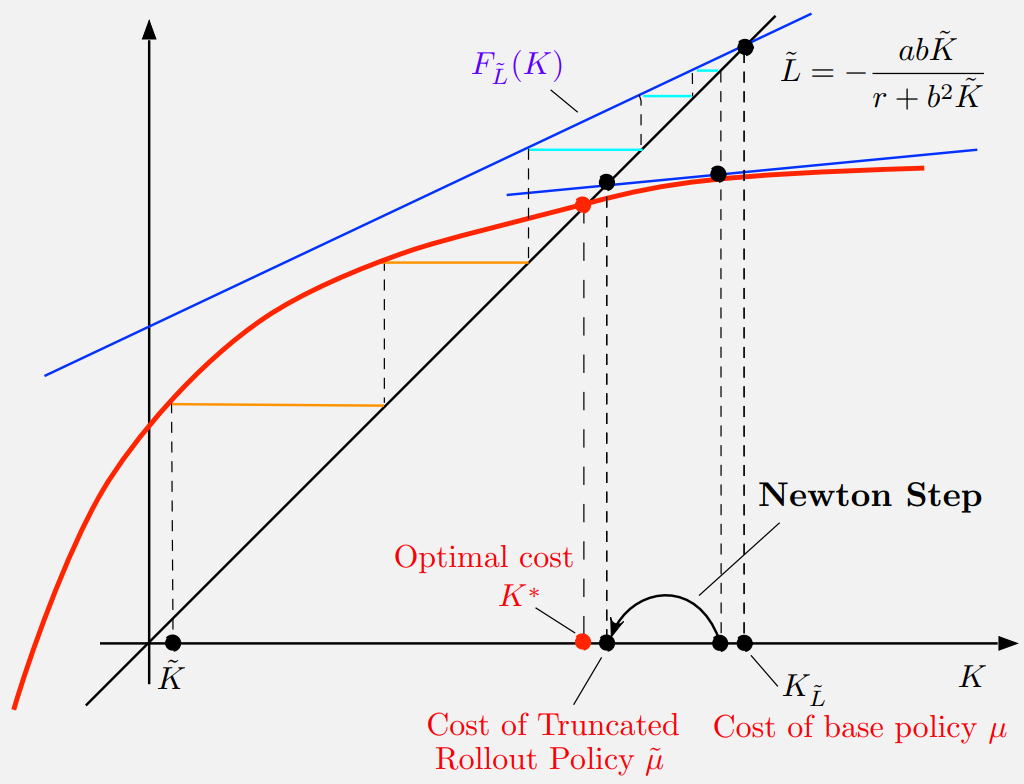

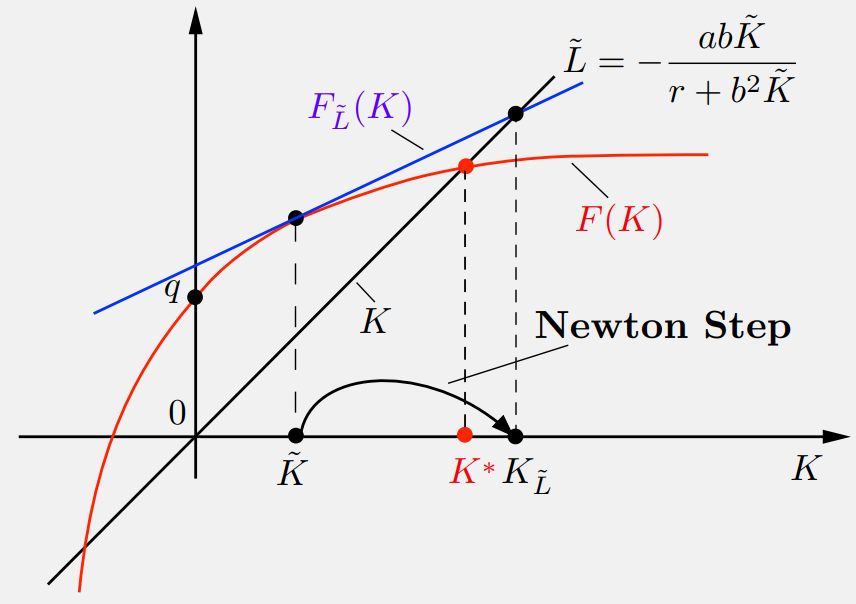

4. Approximation as Newton's Method

Approximation in value space with one-step lookahead can be viewed as a Newton step for solving the Bellman equation.

One-Step Lookahead

Maps a terminal cost approx \( \tilde{J} \) to the cost of the one-step lookahead policy \( \tilde{\mu} \).

This is equivalent to linearizing the Riccati operator \( F \) at \( \tilde{K} \) and solving the linear system.

Fig 3: One-Step Lookahead as Newton Step

Multistep Lookahead

For \( \ell \)-step lookahead, we perform \( \ell-1 \) VI steps (staircase) before the Newton step.

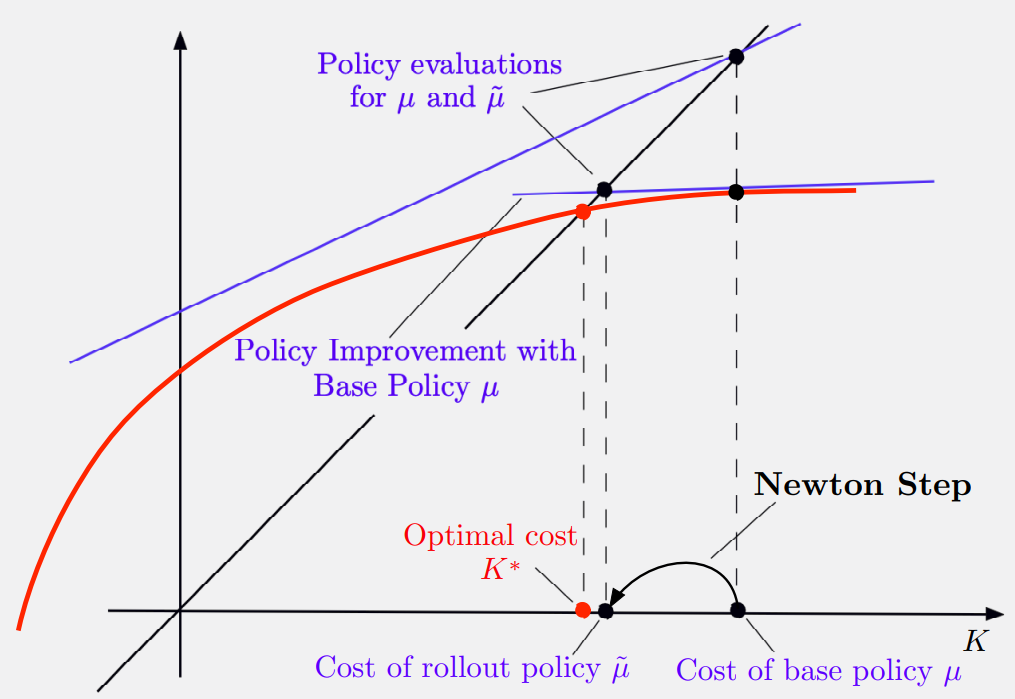

5. Rollout & Policy Iteration

Policy Iteration is simply repeated application of non-truncated rollout.

Quadratic Convergence

For the LQ problem, Policy Iteration (Newton's method) converges quadratically to the optimal cost.

\[ ||K_{k+1} - K^*|| = O(||K_k - K^*||^2) \]6. Test Your Knowledge

1. The Riccati operator \( F(K) \) is:

2. For a stable linear policy \( \mu(x) = Lx \), the cost equation is:

3. One-step lookahead minimization is equivalent to:

4. Policy Iteration convergence rate for LQ problems is:

5. In truncated rollout, we use:

🔍 Spot the Mistake!

Scenario 1:

"The Riccati equation always has a unique solution."

Scenario 2:

"Value Iteration converges in a finite number of steps for LQ problems."

Scenario 3:

"Newton's method is slower than Value Iteration."

Scenario 4:

"Any linear policy is stable."

Scenario 5:

"Rollout is an offline planning method."